Register to get free articles

Want unlimited access? View Plans

Already have an account? Sign in

This year has been defined by a sense that we have finally escaped the clutches of recession. But with China’s growth slowing dramatically and stock markets gripped by panic in recent weeks, some are suggesting we’re on the verge of another, much worse, crash. MICHAEL NORTHCOTT explores where we currently stand, and asks what this will mean for the gold price and the jewellery industry as a whole.[divider style=”solid” top=”20″ bottom=”20″]

It’s 2008, and Northern Rock is facing the largest run on a bank since the Victorian era. Hundreds of people queue outside high street branches as television cameras swarm on the commotion. The media is awash with hysterical doomsday scenario predictions: no money left in the cash machines, employers unable to pay their workers’ wages, the army on the streets.

But naturally in such circumstances, little attention is paid by the mainstream press to smaller industries such as jewellery and what might lie in store for them as a result. Only the banks, construction firms and major export industries are given the analytical run-down by London’s financial journalists. But jewellery – still a multi-billion industry in the UK – faced a cataclysm every bit as real as the quarterly statements of the major financial institutions. For it was those very institutions which, in their panic, began to take refuge in gold.

Jewellers and manufacturers had already been weathering a precipitous decline in sales of precious metal lines, reflected starkly in the official hallmarking figures. The Birmingham Assay Office’s monthly reports gradually painted a picture of arguably the worst decade in history from the beginning of the Noughties, with the number of recorded hallmarks made across the four assay offices falling from over 22 million per year to just 4 million per year. Whether it was down to the now-normal market characteristic of jewellery competing with technology for consumer spend, or because of the rise of global jewellery brands with huge marketing budgets and a penchant for using base metal, the industry here in the UK was suffering well before recession hit.

Then came the bull market. Gold has long been seen as a safe place to stash money by governments, companies and individuals alike, though it is hard to know exactly why it is the commodity of choice – platinum, for example, has similar characteristics. It is in the ‘precious metals stable’, it is rare, expensive and consistently in demand. Still, gold is where the money heads in tough economic times, rhyme or reason aside. But for those in the jewellery industry, it meant that margins on gold jewellery were virtually erased overnight. Why would a customer pay one price for a pendant one year and more for the same item the following year? The answer was, as hallmarking showed, they wouldn’t.

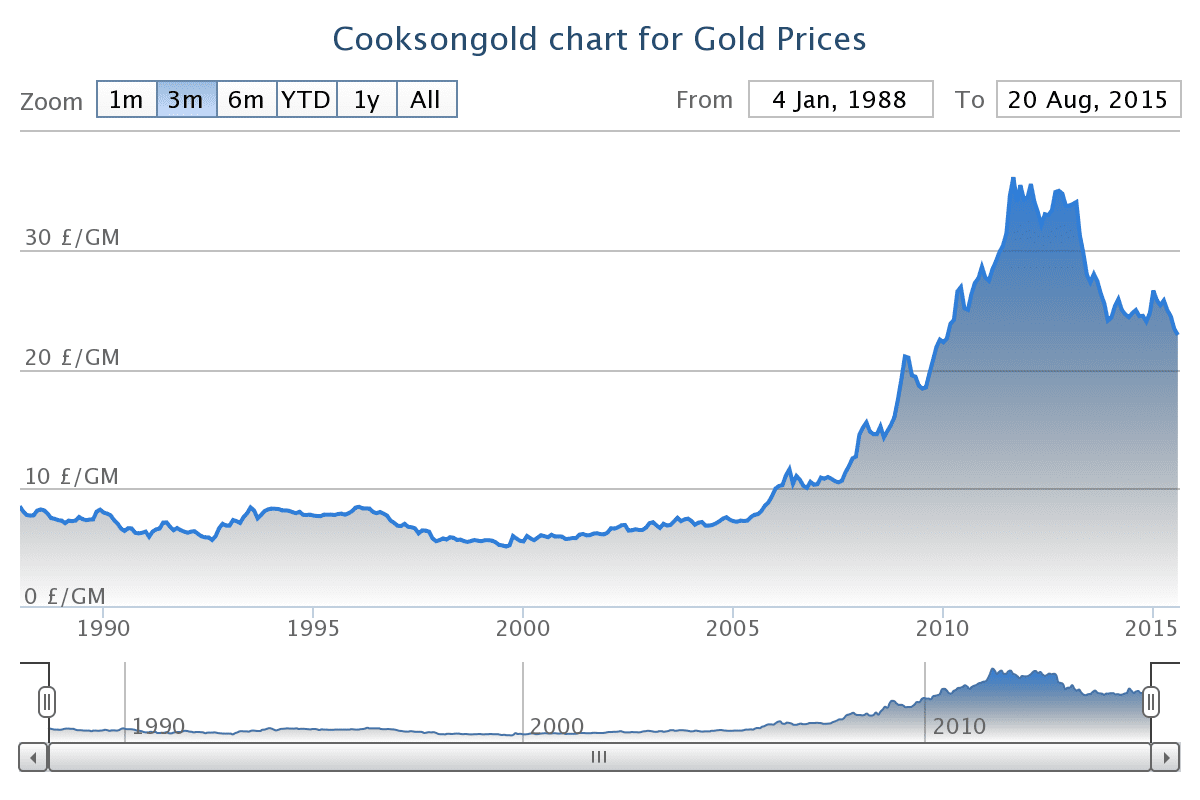

The gold price has reduced to a certain extent since those heady days, but it is by no means back to ‘normal’, still hovering at more than twice pre-2007 prices according to the latest data from Cooksongold. Still, jewellers report they are finding they can shift a little more than before, and manufacturers have been able to start manufacturing slightly heavier pieces once again – as soon as the price returns to manageable levels, the consumer is interested again. Though not back to the good old days, things were genuinely looking rosier.

CHINA PULLS THE PLUG

In the last few weeks, it has become apparent that the global financial situation has, far from being fixed since the late 2000s, shown more cracks. The slowdown in China’s economic growth has caused panic in the stock markets, with the FTSE 100 and other exchanges across the globe posting sharp losses. Being the growth engine of the world has made China a linchpin in world finance. Add to this the collapsing oil and energy prices in the West and the rapid growth of shale gas exploration, and it seems bets that once seemed safe now look riskier than ever. The same can be said of gold.

Gary Williams, managing director at Presman Mastermelt, says the landscape has changed markedly in recent decades. “I remember in the 1980s,” he says, “if someone sneezed in the Middle East, the gold price would rise straightaway. But it doesn’t seem to have the same effect anymore.” He points to the fact that where wars and instability used to be significant enough to affect commodity prices, conflict is now so frequent around the world that prices do not seem to react in the same flighty way. “If the Chinese economy has the effect that people are worried about, then you would think it would push the price up, but within a couple of days of the market wobbling, gold had actually fallen again.”

That uncertainty has partly been precipitated by the high-speed trading practised by institutional investors and modern banking. Apple Nooten-Boom of Hean Studio, points out that it is not worth speculating about the gold price in the jewellery industry. “I think the volatility in the world means you just don’t know what institutional investors are going to do. When they do invest, it is sudden and rapid. They pile into a particular area and push the price up, and then sell at that higher price in large volumes, and the price falls again. They are not interested in making an investment, they are interested in movement – all so they can make a quick profit.”

But if history is anything to go by, and we must consider the possibility that the usual pattern of the gold price soaring may appear again, what will this mean for the jeweller? Nooten-Boom says, functionally, there is nothing to worry about. “We tend to work purely on the basis of ‘what do I need today, what is the price’, and whatever it is, that is my cost base. You keep your stocks to a minimum but you know they can go up and down in value.”

Williams thinks there is something more serious on the horizon. “I think margins today are tighter than they have ever been. There is much more competition in terms of the number of brands, and e-commerce has put pressure on the bricks-and-mortar margin. The jewellers are only just getting comfortable with the fact that the price has come down a bit.” He says that the two key things that allowed jewellers to muddle through amid this trading environment were “scrap-buying, and Pandora”.

“The worrying thing now is after three or four years of the high gold price and the scrap-buying craze behind us, I don’t think the jewellers can sustain the purchase of scrap at the level needed to keep their business going,” he adds.

WHERE DOES HALLMARKING FIT IN?

Against a backdrop of apparent gold price stabilisation, hallmarking figures have shown promising signs of recovery this year. Almost every month, the figures rose compared with the same period the previous year. On several occasions the rise was in double figures territory. But in July, they dropped by around 10% – a surprise blip in what was otherwise an encouraging trend. Stella Layton, chief assay master at the Birmingham Assay Office says we need to see how the months ahead pan out before we can answer the question of why this drop occurred. “June and July are showing a reduction, yes, but is that poor sales on the high street because of poor summer weather in the holiday season, or is it genuine nervousness in the high street? The jury is still out. We need a September figure before we can analyse this.”

But Layton says the behaviour of the gold price makes it difficult to analyse data in the way we might have done in the past – understandable given that old benchmarks are now turning out to be more variable than previously thought. If the price of gold cannot be relied upon (if not to remain stable then at least to move predictable ways), then how is it possible to tell what is influencing fluctuating hallmarking numbers? “We are not in a stable economic environment. My prediction would have been that gold turned into a bull market [in the wake of the news about China] but it actually seems to have deteriorated in price.”

She takes a different view from Williams on the issue of scrap gold and the extent to which the jeweller will be able to lean on this once again. “There’s still a lot more scrap in our cycle now than there was in, say, 2005, it’s just not as healthy as it was at the peak. The people who actually had to trade the scrap in, traded it in. But I believe there is still a lot more out there, we just don’t have the key to accessing it at the moment.”

WHAT NEXT?

With the gold price hard to follow (much less fully understand), and the global economic situation precarious, the consensus seems to be that margin will not be the issue for the jewellers, more than good old-fashioned decreased spending by middle England. All three industry figures interviewed for this piece were in agreement that fiscal belt-tightening by the middle segment of the market would be more of a threat than institutional investors taking refuge in gold and pushing the price up. And in any case, the data of recent weeks suggests hedge funds and their ilk may not even be keen to do things that way, this time around.

Specifically on the margin point, Williams says accounting for shrinking margins has already been done. “[Jewellers] have had to reduce their margins to stay competitive, and even though they’ve done that, it is now a question of how to entice the consumer to spend with you. If consumers are concerned about their own wallets due to the economic situation, they will just stop spending.”

So is there a doomsday scenario to worry about after all? On the assumption that there is very little we can point to as a reliable indicator of where we’re heading, that notion of muddling through and working day-to-day is perhaps the best philosophy. And as for industry collapse, it’s probably a level of hysteria we should leave to those financial journalists looking at the value of gigantic corporations. In the more modest world of jewellery, as Williams puts it: “The market never dies, it only shrinks.”

FIG 1 – Graph showing the gold price from 1988 – 2015. Note the dramatic increase on the eve of the 2008 recession, and how the current price remains twice as high as the mid-2000s plateau.