Register to get free articles

Want unlimited access? View Plans

Already have an account? Sign in

“In two to five years we won’t be talking about Blockchain, it will just be one of those things that is a given,” says Leanne Kemp. She is CEO of Everledger, a global startup that uses the best of emerging technology including Blockchain, Smart Contracts and Machine Vision to assist in the reduction of risk and fraud for banks, insurers and open marketplaces. “We are a digital global ledger that tracks and protects the provenance of items tracking it from the source to the markets and after two and half years we have begun to show our work to the world in tracking diamonds.”

Kemp has been working at the forefront of digital technologies since the mid-Nineties having started working in Radio Frequency Identification technology (RFID) following years as a software engineer and she believes it is this new wave of technology that can help fight some of the pressing problems the industry is currently facing. “I’ve been a software engineer and have worked in supply chain and track and trade for over 20 years,” she says, “I have bought a diamond myself and when I did I asked the question ‘where is it from?’ and I have experience in being in the jewellery industry since 2007 so the combination of all that together meant I understood what the challenges in industry were.

“I also understood what could be done technically with Blockchain and what other technology could be combined with Blockchain. It is a combination of all these things that will transform the industry and will help solve some of the problems that can’t be solved with the current way of operating.”

Everledger are only one of a number of companies that are racing to be at the forefront of this next-generation technology. Multinational technology company IBM collaborated with a a consortium of gold and diamond industry leaders including Asahi Refining, Helzberg Diamonds, LeachGarner, The Richline Group and UL to launch its own platform TrustChain, while the De Beers Group partnered with diamond manufacturers – Diacore, Diarough, KGK Group, Rosy Blue NV and Venus Jewel to launch its blockchain platform called Tracr.

The pilot project, involving a small group of industry participants, launched in January 2018, following a successful proof-of-concept trial, and is on track for a full launch later this year. De Beers is a major player in various parts of the diamond value chain, providing roughly one-third of the global supply of diamonds by value.

Feriel Zerouki, senior vice president for international relations and ethical initiatives at De Beers, agrees that Blockchain has the potential to revolutionise the level of trust in the industry “by enabling data on diamonds to be recorded in a way that was not previously possible, hence underpinning trust and increasing traceability for consumers and trade participants alike”.

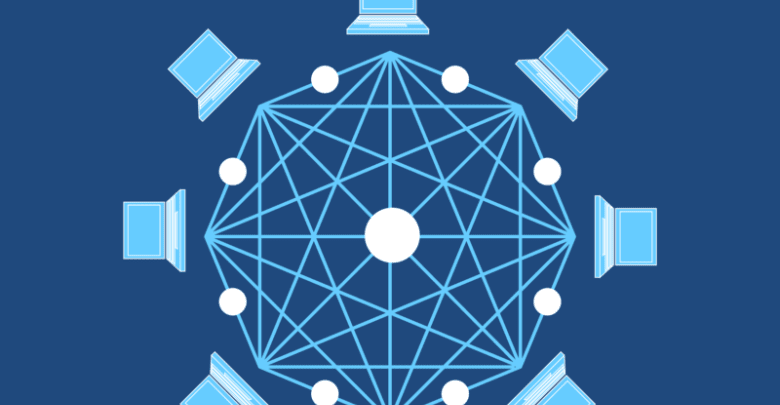

What is Blockchain, and how does it work?

Blockchain itself is a database technology meaning that Blockchain alone won’t actually track anything, it will only track the records that are associated with something. Online Blockchain training platform Blockgeek describe it as a “spreadsheet that is duplicated thousands of times across a network of computers. The network is then designed to regularly update this spreadsheet”. While Blockchain has been around since Satoshi Nakamoto invented Bitcoin in early 2009, its uses outside of the cryptocurrency space were only realised in 2014.

Zerouki describing the process that underpins the Tracr initiative says: “When diamonds move along the value chain, Tracr registers key information and interactions at each stage that become ‘blocks’. Each block must be validated by the blockchain community before it can be added to the blockchain, and the blockchain grows with each new block that is registered. When ‘chained’ together, the blocks will construct a complete digital record for each diamond.”

In more general terms Kemp calls Blockchain a “next-generation internet technology” and infers just as the internet enabled two computers to talk to each other and email enabled two people to communicate to each other, Blockchain is a technology that enables the transfer of value between two people. She also elaborates on its wide reach past that of just the diamond industry: “It is a ledger that the internet will propagate so that you can build a business network of transactions. You can track and trace and transfer value of things. That thing might be digital money, it could be something of value like a diamond and the ownership of that diamond, or it could be a car, or property – whatever you wish.”

That is why Blockchain is seen by many as revolutionary; the technology can work for almost every type of transaction involving value, including money, goods and property. Some are even predicting that it 10 years time it will be used to even collect taxes – its potential uses are almost limitless. “It’s the same thing as in 1989 when we started talking about a thing called the Internet and then all of a sudden everybody was talking about websites and ecommerce,” says Kemp. “Think back to when the internet became popular or cloud computing, and the same thing is happening now. Blockchain is not just for the diamond industry it is the next-generation internet technology, 71 banks are using it which have nothing to do at all with the diamond industry.

“We are already seeing it used with tracking health care records at hospitals; everyone is looking at possibilities and unless an industry decides it doesn’t need the internet anymore or we don’t need mobile phones or email then Blockchain will matter sooner or later. It is clearly something that everyone will consider using. It is not just being talked about for the diamond industry it is being used everywhere. People have finally realised they all need one.”

The potential impact?

Thus Kemp believes that Blockchain is going to be a necessity in the industry in the future, rather than simply a choice. “I certainly think it is an important part of internet technology so companies that have internet enabled or have digital enablement are going to naturally take a hold of this. It will be a tool they would use simply like using a word document.

“Retailers will be able to show the story of their diamond and it is going to be on the merit of manufacturers to want to give that data and accessibility so retailer can do that. The reality is that retailers want it so they are pulling for it and diamond manufacturers want to be able to give it so they can support the growth of industry rather than just the preservation of the industry.”

Zerouki argues that creation of a tamper-proof and permanent digital record for every diamond registered on the platform will establish a single source of data for those diamonds, thus in theory creating new efficiencies in the value chain, reducing the cost of doing business for participants and providing consumers with further assurance that their diamond is natural and conflict-free.

On a retail level Zerouki sees the main advantage as the retailer having the added ability to converse to the consumer about the origins of its diamonds and to encourage consumers who may have avoided the industry over previous ethical concerns. As blockchains are publicly accessible, anyone will have the ability to check the provenance of their stone and have confidence that the record wasn’t altered by any parties attempting to pass off conflict or fake stones as genuine.

“Tracr will allow diamond retailers to enhance their consumer ‘story-telling’ about diamonds.

Retailers will be able to provide consumers with trusted, verifiable information about their diamond and its journey, giving them the confidence that their diamond is natural, sourced from a conflict-free area, and that its physical characteristics match its digital diamond report,” he says.

More importantly, alludes Kemp, it could be used not just to solve problems involving the provenance of diamonds but possibly the financial constriction facing the diamond and mining industry. “The big issue is around transparency of financial institutions and how we can bring transparency to the banks so that can transform, meaning we are then are able to gain better access to finance to finance the industry and the conversion from rough to polished diamonds. I think that is the more important challenge to be solved, because if that can’t be solved the industry is going to shrink, not grow, and only the larger companies will be able to survive as the smaller ones will not be able to track themselves the finance.

“I am currently in Antwerp and [here] we have 800 diamantaires struggling as they can’t even open a bank account to deposit into it let alone borrow money. That is the bigger problem that needs to solved and Blockchain definitely can help solve this.”

The future

The potential impact is already beginning to take hold – Signet Jewellers, the world largest retailer for diamond jewellery, recently became the first to join the Tracr pilot with the partnership initially focusing on expanding the pilot’s scope to cater for smaller-sized goods. CEO Virginia Drosos said of the agreement: “We are joining the Tracr pilot because we believe the project not only has strong potential to facilitate increased transparency and confidence within the industry, but it can also foster much-needed digital transformation.”

Similarly, Everledger announced a partnership with the Hari Krishna Group (HK Group) that will see Hari Krishna’s flagship private label brand ‘My Diamond Story’ tracked using Everledger’s Blockchain technology.

While some may dismiss the early adopters of Blockchain as a marketing gimmick, the jewellery industry is realising, slowly but surely, that Blockchain provides workable solutions to some problems that need solving. he technology living up to its promise of bringing the industry into the future.